2015 • No. 15–8

By Claire Greene and Mi Luo

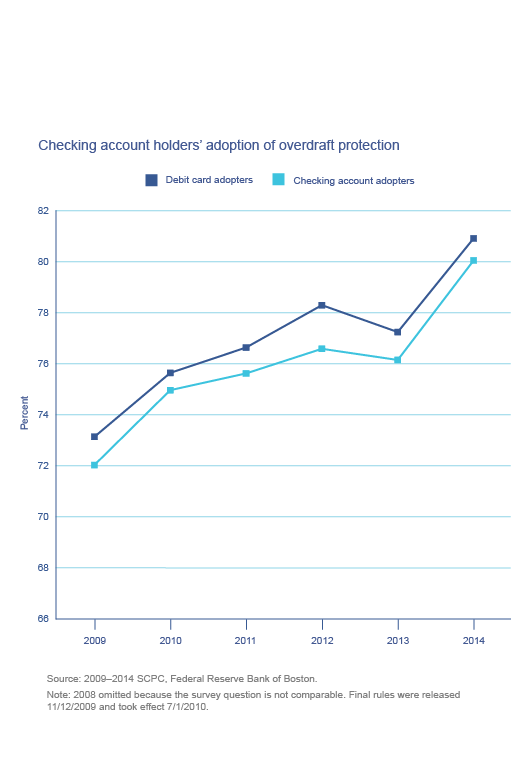

In mid-2010, an amendment was passed to Regulation E, which implements the Electronic Fund Transfer Act, requiring financial institutions to ask consumers whether or not they want overdraft protection for automated teller machine (ATM) transactions and everyday purchases made with a debit card. This Research Data Report studies the short-term impact of this amendment by examining consumers’ adoption of overdraft protection, the incidence of overdrawing at least once within a 12-month period, and the incidence of paying a fee for overdrawing, before and after the opt-in rule took effect.