Consumer payment behavior is a complex intersection of supply-side factors, such as cost, technology, regulation, and merchant acceptance, and demand-side factors, including individual consumer demographics and income, consumer preferences, consumers' assessments of payment method attributes, and network effects stemming from the behavior of peers.

Although explaining the exact causes of payment patterns is challenging, there exists both theoretical and empirical literature addressing many of those factors. The studies summarized in this paper use a growing number of available data sources, including several surveys and diaries of consumer behavior conducted in the United States and elsewhere. Nevertheless, more work needs to be done to understand not just how consumers make their payment choices, but why they pay as they do.

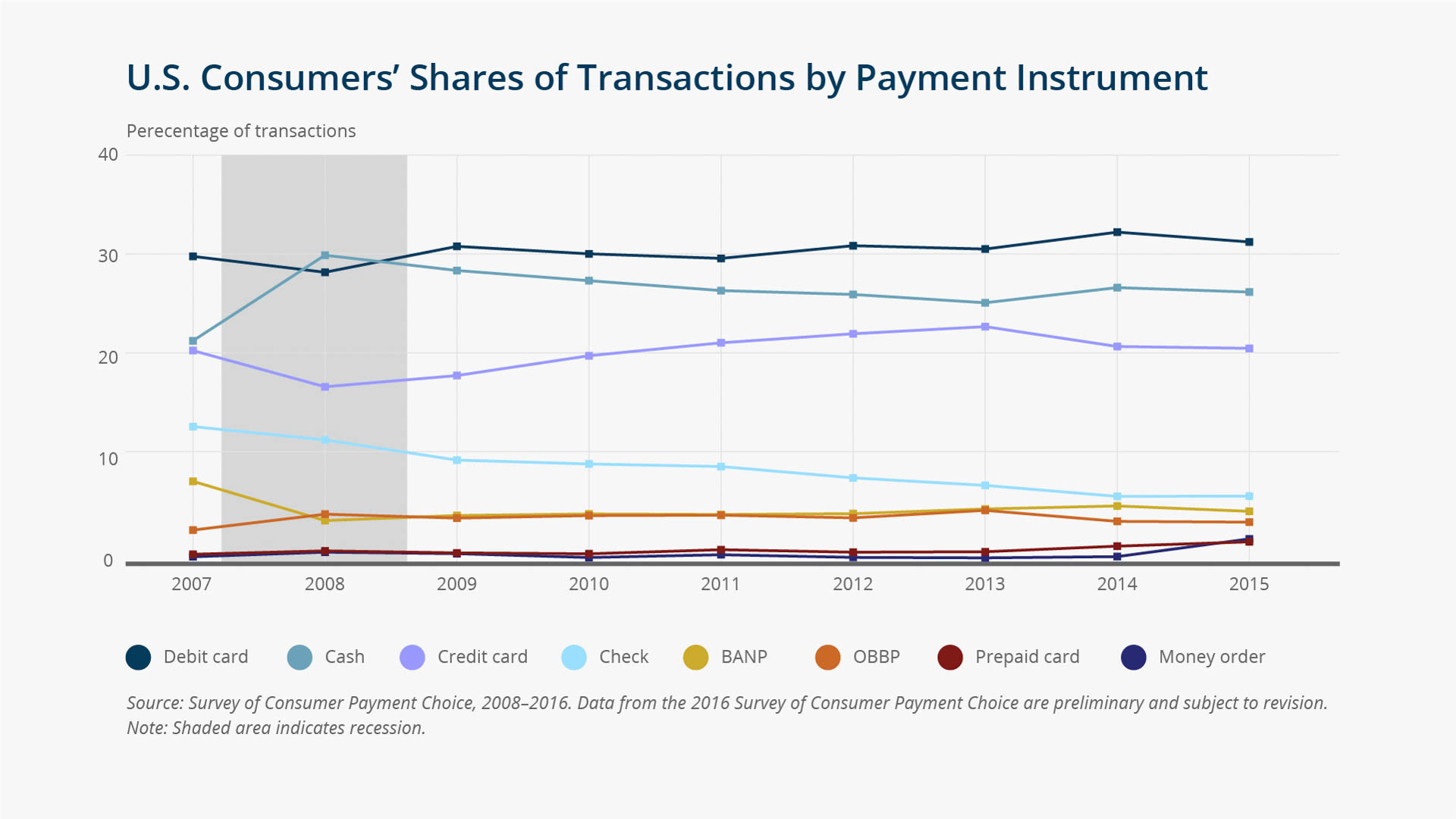

Payment transformation has generated a shift from paper to cards and electronic payments in the United States, but there is also a large degree of heterogeneity among consumers in how they pay. We present factors affecting consumer payment behavior, show data on how consumers pay in the United States, and summarize existing literature on consumer payment choice. On the supply side, technology, regulation, and cost affect payment behavior. On the demand side, consumer demographics and income, consumer preferences, and consumer assessments of payment method attributes have all been found significant. We focus on price differentiation by payment method by merchants and the effect of such price incentives on payment method use, and on the effect of demographics and of perceptions of payment characteristics on consumer payment choice, emphasizing the effect of security. The studies mentioned here utilize a growing number of data sources, including several surveys and diaries on consumer behavior conducted in the United States and in other countries. We also identify gaps where more research is needed to understand consumer payment choices.