The Southeast Purchasing Managers Index (PMI) report, released on July 5, showed that manufacturing activity in the Southeast rebounded from a less-than-spectacular May. If you'll recall, May's PMI reading was heading in the wrong direction. The overall index had fallen to its lowest level this year, and new orders and production also appeared to be falling, but June's Southeast PMI got us back on the right track.

The Atlanta Fed's research department uses the Southeast PMI to track regional manufacturing activity. The Econometric Center at Kennesaw State University produces the survey, which analyzes current market conditions for the manufacturing sector in Alabama, Georgia, Florida, Louisiana, Mississippi, and Tennessee. The PMI is based on a survey of representatives from manufacturing companies in those states and analyzes trends concerning new orders, production, employment, supplier delivery times, and inventory levels. An index reading above 50 indicates expanding activity, and a reading below 50 indicates contracting activity.

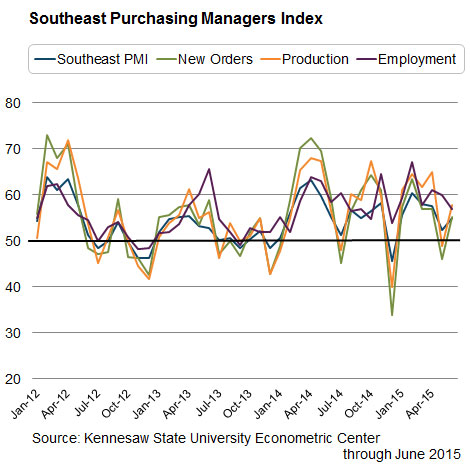

The PMI index rose 2.7 points in June to 55.1 from May's 52.4 (see the chart). Most of the subindexes indicated positive movement as well, particularly new orders and production.

- The new orders subindex rose 9.3 points to 55.3, after falling into contractionary territory in May.

- The production subindex increased 8.9 points compared to the previous month and now reads 57.9.

- The employment subindex declined 3.0 to 57.0.

- The supplier deliveries subindex decreased 3.4 points to 52.6.

- The finished inventory subindex increased 1.6 points to 52.6.

- The commodity prices subindex fell 1.4 points and now reads 52.6.

The rise in the overall index is welcome news, but even more welcome are increases in the new orders and production subindexes. The new orders subindex is the most forward-looking indicator in the survey. When new orders fall, it generally suggests that future demand for manufacturing products may be weakening and future production may be lower. As a result, employment levels at manufacturers could also decline. It would normally take several months of subpar activity for this to occur, and a one-month drop is nothing to get excited about. Still, it is always nice to rebound quickly. June's report will hopefully set the stage for a strong third quarter.

By Troy Balthrop, a Regional Economic Information Network analyst in the Atlanta Fed's Nashville Branch