The availability of affordable housing in the Southeast is an increasing challenge, especially in areas of opportunity that have jobs, good schools, public transit, and so forth. The Atlanta Fed's Community and Economic Development discussion paper "Declines in Low-Cost Rented Housing Units in Eight Large Southeastern Cities" puts some numbers to the depth of the problem, with metro Nashville showing a loss of over 7,700 low-cost rental units between 2010 and 2014.

In light of these challenges, sources of funding for affordable housing are more important, and competitive, than ever. One of the best-known and most competitive sources of funding for affordable housing construction is the Low-Income Housing Tax Credit program, or LIHTC. The most common form of the program, the 9 percent credit, is already a highly sought-after affordable housing construction subsidy, but LIHTC also offers a noncompetitive 4 percent tax credit. This 4 percent credit, typically paired with the development of affordable housing financed with state or local government-issued tax-exempt bonds, is a less often utilized financing strategy and still an important tool in the affordable housing tool kit (Novogradac, 2016e).

Until now, the main reason for the 4 percent credit's limited use is that the combination of tax-exempt debt and the equity attracted into affordable housing development through 4 percent credits is insufficient to cover the cost of development, thereby requiring developers of affordable housing to seek an additional subsidy from public and philanthropic sources. This challenge is only being exacerbated by pricing trends in the market today. The current debate over corporate tax reform has resulted in reduced demand for (and therefore the value of) tax credits by 10 cents to 15 cents per dollar (Kimura, 2017). Less demand for tax credits pushes down the price per credit, resulting in a larger financing gap on tax credit financed affordable housing.

However, the 4 percent LIHTC program's underutilization and current pricing trends combine to present an opportunity for community and economic development practitioners to work with affordable housing developers to ensure that good money to support affordability isn't left on the table. A broad alliance of CED professionals armed with an understanding of the technical aspects of the 4 percent LIHTC program may be the key for unlocking more subsidy that supports affordable housing.

What is LIHTC?

The LIHTC is the largest supply-side affordable housing subsidy in the nation. Created in the 1986 Tax Reform Act, the LIHTC program has housed nearly 13.3 million people over its 30-year lifespan by subsidizing the construction or substantial rehabilitation of housing units affordable to persons making either 50 percent or 60 percent of their area's median income1 (Novogradac, 2016c).  Its $8 billion annual allocation authority is divided up among all 50 states, Washington, DC, Puerto Rico, and the U.S. Virgin Islands. It is allocated to private or nonprofit developers on a competitive basis as defined by each state's qualified allocation plan (QAP).

Its $8 billion annual allocation authority is divided up among all 50 states, Washington, DC, Puerto Rico, and the U.S. Virgin Islands. It is allocated to private or nonprofit developers on a competitive basis as defined by each state's qualified allocation plan (QAP).

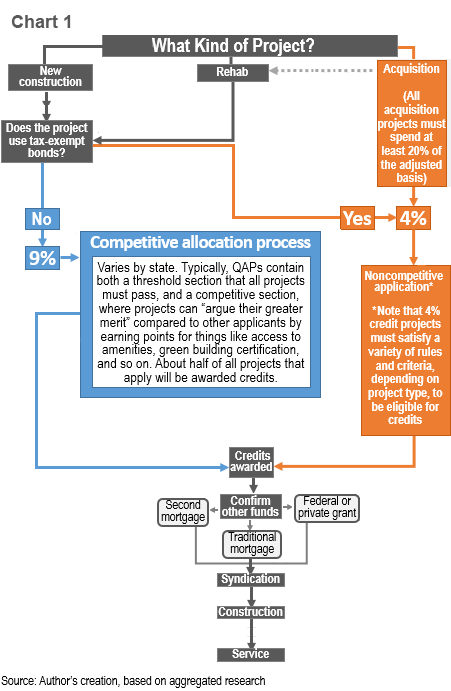

The program operates through a financial mechanism in which a development entity earns tax credits for eligible construction/rehab activities, and in turn transfers those credits to an investor (a process known as syndication) in exchange for capital needed to complete the project (see chart 1). Once built, the housing must remain affordable, with rents at or below 30 percent of the selected area median income cap for the affordable period, typically 30 years. For the first 10 years, the investor gets to claim 1/10th of the total credits, reducing the tax liability for that year (Novogradac, 2016a).

Why are there 9 percent and 4 percent options?

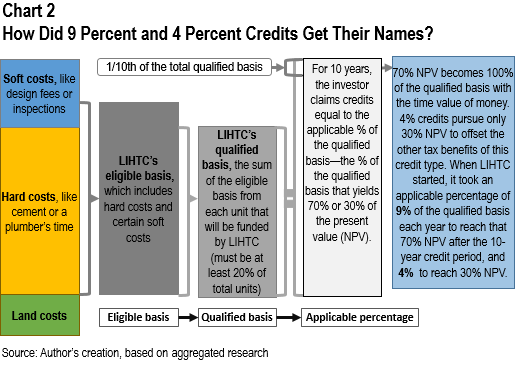

The 9 percent and 4 percent credits relate to LIHTC's unique financial mechanism. Each housing project constructed or rehabilitated has a variety of costs associated with it, divided into land costs, hard costs such as lumber or a plumber's time, and soft costs such as administration expenses or consultant fees (IRS, 2015). Most hard costs and some soft costs form the eligible basis—the elements of a project that can be financed by LIHTC. Then, the eligible basis is multiplied by the fraction of units within the project that are set aside to be affordable under LIHTC, resulting in the qualified basis (IRS, 2015).

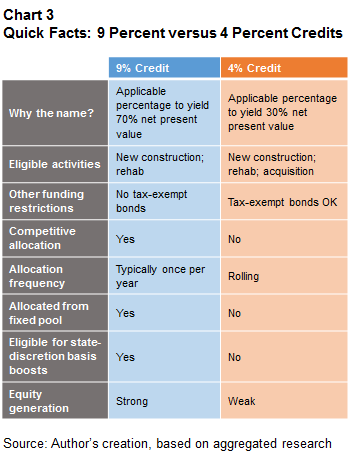

The tax credit that an investor can claim each year is determined by the applicable percentage of the qualified basis. That percentage is the rate that, over the 10-year return period, yields 70 percent of the net present value, henceforth referred to as NPV, of a new or rehabbed building that is otherwise not federally subsidized, or 30 percent of all other buildings (IRS, 2008). The applicable percentages to achieve that goal have historically varied somewhat month to month, but initially hovered near 9 percent and 4 percent, respectively—this is how the 9 percent and 4 percent credits get their names (see chart 2).2

How does the 9 percent credit work?

Each year, states are given allocation authority over a fixed amount of 9 percent credits, according to an inflation-adjusted, population-based formula. In 2016, states received $2.35 per person or $2.69 million, whichever was greater, to award to proposed affordable housing projects (Novogradac, 2016d).

In order to determine which projects will be awarded the 9 percent credits, states hold a competitive application round, generally once or twice per year. Interested developers submit an application according to the standards and requirements listed in each state's QAP, and the state Housing Finance Agency or its equivalent evaluates the application. Many states divide their QAPs into threshold (mandatory) and competitive sections, with developers seeking as many competitive points as possible through provision of amenities such as transit access or community rooms. Competition for 9 percent credits tends to be highly competitive.

What projects qualify for a 4 percent credit?

Two types of projects qualify for a 4 percent credit: (1) acquisitions, and (2) projects (new or rehab) that use tax-exempt bonds. The idea behind the 4 percent credit for acquisitions is that only the changes needed to convert the ownership and reserve the selected units for lower-income tenants should be subsidized. Projects that receive an additional federal subsidy are, for LIHTC purposes, those that are debt financed using tax-exempt bonds. This provision is intended to create greater financial parity between projects financed with commercial debt and those financed with public bonds that are exempt from taxation. In practice, affordable housing projects that rely on tax-exempt bonds are typically intentionally structured to take advantage of the "automatic" 4 percent credit (see chart 3 for a quick comparison of the two credits).

What are some benefits and challenges of each type of credit?

The 9 percent credit is allocated by each state on a competitive basis, and typically at fixed points during the year. By contrast, 4 percent tax credits are allocated on a noncompetitive, rolling basis. This offers projects seeking 4 percent credits greater flexibility in terms of timing and a much better chance of successfully gaining an award.

However, 4 percent credits rarely generate sufficient equity to close the financing gap remaining on a tax-exempt-bond-financed development, particularly compared to their 9 percent counterparts. This issue is caused by the lower applicable percentage, which reduces the total purchase price of credits even if the price per credit stays the same. The lower price produces a financing gap, requiring the project to seek additional funding through grants or other subsidies. This gap can also increase the foreclosure or failure risk of a project, since the level of leveraging is much higher than in 9 percent credit projects.

In addition, complex policies and transaction costs sometimes create headwinds to financing affordable housing with 4 percent credits. Not all states use their private-activity bonding authority for housing in all years (IRS, 2016), and when they do, demand may exceed volume available (Novogradac, 2014b). Also, tax-exempt bond projects receiving 4 percent credits must also obey the "50 percent rule," which governs the distribution and uses of the capital stack (see Mullen, 2006; Smith, 2009 for a detailed explanation of this rule), and at least 15 percent of bond funds must be used for rehab if the project is for an existing building. Finally, due to the complicated funding process and many rules surrounding the bond and 4 percent credit processes, there are often relatively high financing fees associated with the credits (Smith, 2009).

Despite these complications, the vast majority of affordable housing projects seeking to attract debt through tax-exempt bonds do succeed in obtaining 4 percent credits, leading some professionals to say these credits are automatic.

How do organizations close the financing gap?

Organizations close the financing gap in a variety of ways, depending on the type of project, the development partners, and the particulars of each deal. In general, many nonprofit developers seek additional grant funding, either from private philanthropies or through government grant-making bodies, which are typically local or state agencies allocating state or federal funds.

Programs often used for this kind of financing include HOME and CDBG funds made out of state or city allocations, or Federal Home Loan Banks' Affordable Housing Program grants made through a member bank. For example, Michigan created a program explicitly for 4 percent credit gap financing, using a combination of HOME and preservation funds, in the form of a low-rate second mortgage (Michigan State Housing Development Authority or MSHDA, 2013).

Projects financed with 4 percent credits and tax-exempt bonds may also require additional sources of debt. Historically, borrowers have sought below-market or tax-exempt loans from federal sources such as the Federal Housing Authority (Coate, 2013). More recently, some deals have taken on taxable conventional mortgages due to the unusually low interest rates currently offered, faster processing time, and concerns over municipal credit quality (Gerwitz, 2013; Toker, 2011). These mortgages may come from commercial lenders or government-sponsored enterprises like Freddie Mac, which recently launched an attractive new instrument as part of its program to finance more very low-income units (Freddie Mac, 2015). Additionally, other innovative new loan structures like hybridized bond loans have recently emerged for these deals, offering yet more ways of closing the financing gap for 4 percent credit projects.

Historically, the 4 percent LIHTC credit has been underutilized as a source of affordable housing finance. Despite its advantages and flexibility, the combination of tax-exempt debt and the equity attracted into affordable housing with 4 percent tax credits is insufficient to cover the cost of development. This in turn forces developers to seek an additional subsidy from local governments, philanthropy, and/or mission-oriented investors. However, the program's underutilization may present an opportunity for community and economic development practitioners to work with affordable housing developers to ensure that money to support affordability doesn't go unused.

By Chris Thayer, CED intern

The author wishes to thank Philip Gilman and Fenice Taylor of the Georgia Department of Community Affairs as well as David Jackson with the Atlanta BeltLine Partnership for their expert consultation on this article. All errors remain the author's.

References

Biber, Joe. (2007, October). "Financing Supportive Housing with Tax-Exempt Bonds and 4% Low-Income Housing Tax Credits." Corporation for Supportive Housing. Retrieved from http://www.csh.org/wp-content/uploads/2012/01/Report_financing-withbondsand-litch_1012.pdf

Coate, B. (2013, December 13). "Closing the Gap: Soft Funding Options for LIHTC Projects." Lancaster Pollard. Retrieved from http://www.lancasterpollard.com/NewsDetail/TCI-Nov-2013-Dec-2014-hsg-closing-the-gap-for-LITHIC-projects

Freddie Mac. (2015, August). Bond Credit Enhancement with 4% LIHTC. Retrieved from http://www.freddiemac.com/multifamily/product/pdf/bcewith4lihtc.pdf

Gerwitz, R. (2013, November). "Four Percent LIHTC Developments Take Advantage of Unusually Low Taxable Mortgage Rates." Novogradac Journal of Tax Credits IV (XI). Retrieved from http://www.citibank.com/icg/sa/citicommunitycapital/docs/novogradac_1113.pdf

Immergluck, D., Carpenter, A., and Lueders, A. (2016, May). "Declines in Low-Cost Rented Housing Units in Eight Large Southeastern Cities." Atlanta Fed Community and Economic Development Discussion Paper 2016-3. Retrieved from https://www.frbatlanta.org/community-development/publications/discussion-papers/2016/03-declines-in-low-cost-rented-housing-units-in-eight-large-southeastern-cities-2016-05-10.aspx

IRS. (2008). "Applicable Percentage under Section 3002(A)(1) of the Housing Assistance Tax Act of 2008." Internal Revenue Bulletin 2008-49. Retrieved from https://www.irs.gov/irb/2008-49_IRB/ar09.html

IRS. (2015, August 11). "Low-Income Housing Credit—Part III Eligible Basis." IRS. Retrieved from https://www.irs.gov/businesses/small-businesses-self-employed/irc-42-low-income-housing-credit-part-iii-eligible-basis#7874

IRS. (2016, September 28). "SOI Tax Stats—Tax-Exempt Bond Statistics." Retrieved from https://www.irs.gov/uac/soi-tax-stats-tax-exempt-bond-statistics

Kimura, D. (2016, October 26). "Borrower's Market." Housing Finance. Retrieved from http://www.housingfinance.com/finance/borrowers-market_o --. (2017, February 14). "Big Changes Jolt LIHTC Market." Housing Finance. Retrieved from http://www.housingfinance.com/finance/big-changes-jolt-lihtc-market_o

Low-income Housing Credit, 26 U.S.C. § 42 (2016). Retrieved from https://www.law.cornell.edu/uscode/text/26/42

Michigan State Housing Development Authority (MSHDA). (2013, September 25). "Rental Development Notice of Funding Availability and General Guidelines for Gap Financing Program." Retrieved from http://www.michigan.gov/documents/mshda/MSHDA-Gap-Financing-NOFA-Update-FINAL_435309_7.pdf

Mullen, B. (2006, May 1). "How to Use Bonds in LIHTC Deals." Housing Finance. Retrieved from http://www.housingfinance.com/finance/how-to-use-bonds-in-lihtc-deals_o

Norris, R. W. & Eichner, R. A. (2013, August 1). "Introduction to Tax-Exempt Multifamily Housing Bonds." Eichner & Norris LLC. Retrieved from http://www.enbonds.com/pdf/09-12-03%20Intro%20to%20Tax-Exempt%20Multifamily%20Housing%20Bonds.pdf

Novogradac, M. (2014a, August 14). "NCSHA Data Reveals Growth in LIHTC Allocations and Units Produced." Notes from Novogradac. Retrieved from https://www.novoco.com/notes-from-novogradac/ncsha-data-reveals-growth-lihtc-allocations-and-units-produced

Novogradac, M. (2014b, September 11). "Housing Solutions: What Role Should Affordable Multifamily Housing Bonds Play?" Notes from Novogradac. Retrieved from https://www.novoco.com/notes-from-novogradac/housing-solutions-what-role-should-affordable-multifamily-housing-bonds-play

Novogradac, M. (2016a). "LIHTC Lexicon." Affordable Housing Resource Center. Retrieved from https://www.novoco.com/resource-centers/affordable-housing-tax-credits/lihtc-basics/lihtc-lexicon

Novogradac, M. (2016b). "Tax Credit Percentages 2016." Affordable Housing Resource Center. Retrieved from https://www.novoco.com/resource-centers/affordable-housing-tax-credits/data-tools/tax-credit-percentages-2016

Novogradac, M. (2016c, February 15). "Celebrating the Low-Income Housing Tax Credit's 30th Anniversary." Notes from Novogradac. Retrieved from https://www.novoco.com/notes-from-novogradac/celebrating-low-income-housing-tax-credits-30th-anniversary

Novogradac, M. (2016d, April 6). "IRS Population Figures Mean LIHTC, Bond Cap Increases for Most States." Notes from Novogradac. Retrieved from https://www.novoco.com/notes-from-novogradac/irs-population-figures-mean-lihtc-bond-cap-increases-most-states

Novogradac, M. (2016e, September 12). "How to Unleash Underutilized Private Activity Bonds to Build More Affordable Rental Housing." Notes from Novogradac. Retrieved from https://www.novoco.com/notes-from-novogradac/how-unleash-underutilized-private-activity-bonds-build-more-affordable-rental-housing

Novogradac, M. (2016f, October 18.) "IRS Data Reveal More Robust Multifamily Bond Market than CDFA." Notes from Novogradac. Retrieved from https://www.novoco.com/notes-from-novogradac/irs-data-reveal-more-robust-multifamily-bond-market-cdfa

Smith, D. (2009, March 6). "Tax-Exempt Housing Bond Basics." IPED Conference. Retrieved from http://www.ipedconference.com/powerpoints/tax-exempt_housing_bond_basics.pdf

Toker, R. (2011, April). "LIHTC Rehabs: Purchasing Properties for Rehabilitation with Low-Interest Loans." Bocarsley Emden. Retrieved from http://www.bocarsly.com/BE_Article_p4.pdf

Zeffert & Associates. (2016). "Managing LIHTC Compliance: Acquisition/Rehab Basics." Retrieved from http://www.mhdc.com/pmc/2016/a/Acquisition%20Rehab.pdf

_______________________________________

1 That is, the building must set aside a minimum of either 40 percent of units for households making 60 percent of area median income (AMI), or 20 percent of units for households making 50 percent of AMI.

2 Note: "funded by LIHTC" here serves as an umbrella term referring to units occupied by LIHTC-qualified tenants, for which the investors can claim credits, based on the lesser of unit fraction or square footage fraction. This chart describes the origins of the two credits' names only and does not reflect the exact functioning of the current LIHTC process.