Construction and Real Estate Survey Results

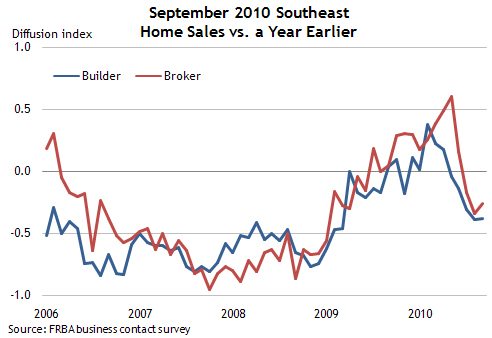

Reports from Southeastern brokers and builders indicated that home sales remained weak in September on a year-over-year basis.

- The majority of brokers continued to note declines on a year-over-year basis. Florida brokers, who had noted more moderate declines in August, indicated that sales weakened further on a year-over-year basis. Elsewhere in the District, sales growth declines moderated.

- Comments from Florida brokers indicated that the recent bank foreclosure halt had stalled many sales; REO sales are a significant share of sales in Florida.

- The majority of brokers and builders reported that home sales were flat to slightly down from August to September.

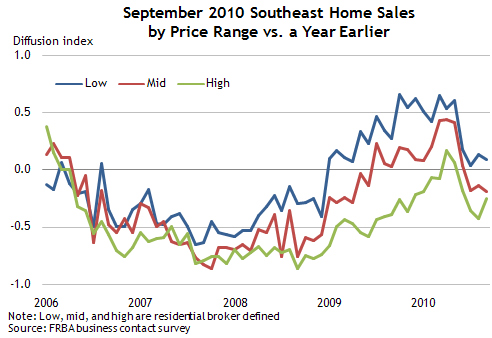

Brokers in the Southeast indicated that home sale declines at the high end of the market moderated while sales growth weakened in the middle and low end of the market.

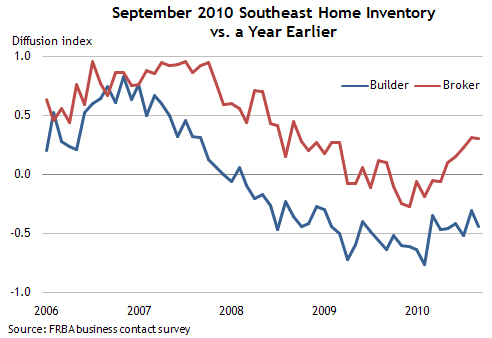

Southeastern brokers said that existing home inventories held steady while builders reported that new home inventories softened on a year-over-year basis.

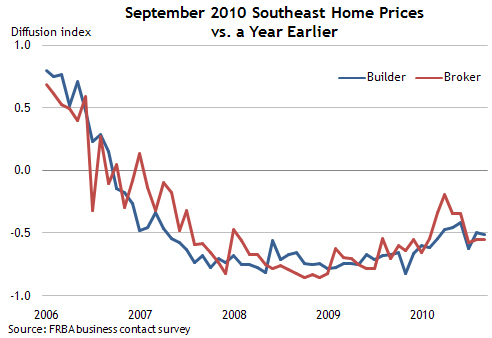

Both Southeastern brokers and builders indicated that home price growth held steady in September, but comments suggested mounting downward pressure on home prices.

Buyer traffic in the Southeast remained weak.

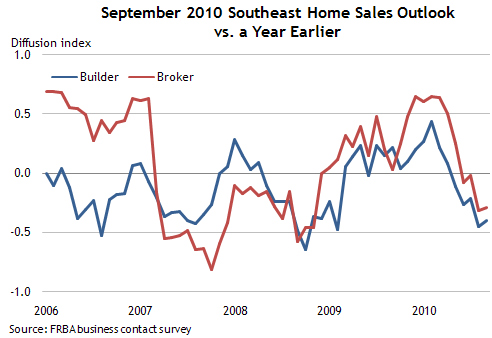

The outlook for sales growth over the next several months indicated a modest improvement according to both brokers and builders.

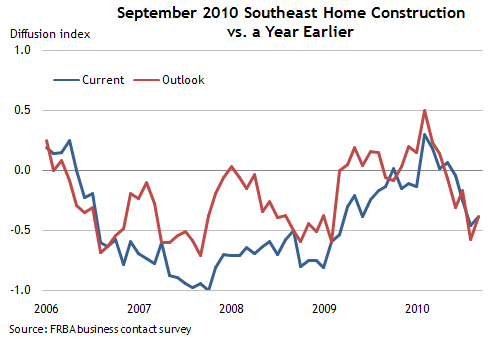

Southeastern builders reported that home construction activity declines moderated in September on a year-over-year basis. The outlook improved slightly as well, but declines are expected to persist.

Note: September survey results are based on responses from 143 residential brokers and 51 builders and were collected October 4–13.

The housing survey's diffusion indexes are calculated as the percentage of total respondents reporting increases minus the percentage reporting declines. Positive values in the index indicate increased activity while negative values indicate decreased activity.

The District Retail Survey showed continued slow activity in the retail sector for September; however, the outlook was more optimistic than in recent months.

- Most respondents reported that activity in September was at or below what they had planned for, and compared to September 2009, sales were mixed. Respondents noted that low-end products were strong sellers last month.

- For the second consecutive month, most survey respondents were positive about the outlook, with 56 percent expecting sales to increase in the next three months.

- In addition, the majority of retailers expect holiday sales will improve from last year.

Note: September survey results are based on responses from 25 retailers and were collected October 4–13.

The retail survey's diffusion index is calculated as the percentage of total respondents reporting increases minus the percentage reporting declines. Positive values in the index indicate increased activity while negative values indicate decreased activity.