In recent decades, technological advances have changed the back-office clearing and settlement of retail payments. Those advances have saved costs, improved funds availability, and paved the way for new payment forms.

For example, a new era in check processing came after the September 11, 2001, terror attacks. The nation's aviation system was suspended for several days, preventing paper checks worth billions of dollars from moving across the country for settlement. Retail Payments Office officials had to pull together a temporary network of trucks to transport as many checks as possible. The air-travel halt exposed weaknesses and inefficiencies in the nation’s check-clearing system, which could have affected the nation’s financial and economic stability and resilience.

The Fed's Board of Governors worked with the banking industry, consumer groups, and other check-clearing networks to draft federal legislation called the Check Clearing for the 21st Century Act, which took effect in 2004. The law, also known as Check 21, allowed financial institutions to convert paper checks into an electronic image that could later be printed as a substitute check to serve as a legally negotiable version of the original paper check. By eliminating the need to transport a check from a bank where it was deposited to one that paid it, the law ushered in the age of electronic check processing and remote deposits. It also reduced the number of days required for check clearing and settlement. Check 21 provided a tremendous boost to the electronic collection of retail payments.

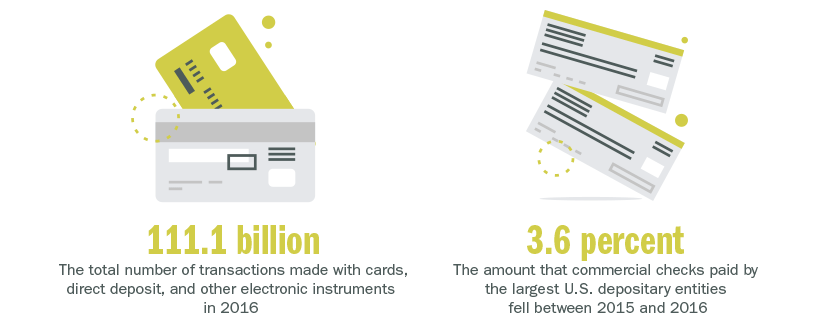

As payment with cards, direct deposit, and other electronic instruments has accelerated, the number of checks written has declined. For example, the number of payment card transactions came to 111.1 billion in 2016, up 7 percent from 103.5 billion a year earlier, according to a 2017 Federal Reserve Payments Study update. During the same time, the number of commercial checks paid by the largest U.S. depository entities fell 3.6 percent.

In 2015, checks accounted for 13.4 percent of noncash payments, down from 57.8 percent in 2000. General-purpose credit and debit cards now make up a greater share of retail payments, accounting for more than 65.5 percent of noncash transactions in 2015.

"There are more things to buy, and how we buy them has evolved and changed," Atlanta Fed senior vice president Jeff Devine said.